.png)

How to Find a Law Firm Bookkeeper Who Actually Understands Legal Accounting

- Nov 3, 2025

- 11 min read

By Chelsea Williams, Chief Financial Architect at Core Solutions Group

Specialized in law firm financial management with 10+ years serving law firms

Key Takeaways

Finding the right bookkeeper for your law firm requires specialized expertise in trust accounting and IOLTA compliance—not just general bookkeeping skills. Generic bookkeepers lack the legal-specific knowledge needed to protect your license and manage attorney trust accounts properly. This guide provides the critical questions to ask, red flags to avoid, and a proven framework for vetting bookkeeping services that understand the unique financial complexities of running a law practice.

You know that gut-dropping moment when you realize your books are a mess?

Maybe it's when you're scrambling to pull financials for a loan application. Or when you discover your trust account hasn't been reconciled in six months. Or worse, when you get notice of a bar audit and realize you have no idea what your bookkeeper has actually been doing.

That moment of panic is your wake-up call.

If you're searching for bookkeeping services for law firms, chances are you're in one of three situations:

The Three Types of Law Firm Owners Looking for Bookkeeping Help

Situation 1: Your bookkeeping is nonexistent.

Hey, no judgment here. You've been focused on building your practice, winning cases, and keeping clients happy. But now the financial chaos is catching up with you, and it's time to face the music. The good news? Your numbers have so much to tell you and will serve as your compass once you get to know them.

Situation 2: You're doing your own bookkeeping.

You've realized that DIYing the books is a mistake when you don't understand accounting principles. After all, garbage in = garbage out. When it comes to law firm accounting and financial management, you DO NOT want to make business decisions based on bad data. Bookkeeping is far from the highest and best use of your time and one of the smartest positions to outsource.

Situation 3: You've realized your current bookkeeper isn't cutting it.

Oh, the stories we could tell you about trust accounting errors that go YEARS back when law firm owners work with bookkeepers who don't understand the nuances of legal bookkeeping. We're talking about compliance nightmares that could have cost them their licenses.

Regardless of what brought you here, we're offering guidance on how to find a law firm bookkeeper who actually understands what they're doing.

Want the complete checklist for hiring and vetting bookkeepers? Download our free Bookkeeper Hiring Checklist to ensure you ask all the right questions and avoid costly mistakes.

Why Finding the Right Bookkeeper Is Critical for Your Law Firm

The highest and best use of time when it comes to your law firm finances is spent wearing your CFO hat, not your bookkeeping hat.

Let that sink in.

You should be analyzing your numbers, making strategic decisions, and planning for growth, not categorizing transactions in QuickBooks at 11 PM on a Saturday night.

But here's what most law firm owners don't realize: not all bookkeepers are created equal. And when it comes to law firm bookkeeping, using a generic small business bookkeeper is like asking your family doctor to perform heart surgery. Sure, they're both doctors, but the specialization matters.

The #1 Non-Negotiable Requirement: Trust Accounting Expertise

If you'd like to keep your license to practice law, this is your number one requirement for a bookkeeper.

You guessed it: trust accounting.

The number of law firms who come to us because their bookkeeper has been with them for years but never understood trust accounting is genuinely scary. We're talking about:

Years of trust accounting errors

Tens of hours spent data mining through transactions

Trying to remember what payments were for when you can't even remember what you ate last week

Had these firms been audited before we cleaned up the mess, they would have surely faced suspension or worse.

Here's what you need to understand about trust accounting: it's universal for bookkeepers who specialize in legal bookkeeping. We recognize transactions when they show up in the IOLTA bank account. But what you need to know is that you're responsible for leaving us data crumbs so we can piece the puzzle together.

You do this by:

Keeping up with your practice management software

Maintaining proper documentation

Leaving notes for your bookkeeper on invoices, check memos, and software platforms

Bookkeepers only know what you tell them about trust transactions, so make sure you and your team are providing all the necessary data.

The Questions You MUST Ask Every Potential Bookkeeper

Don't walk into these conversations blind. Here are the critical questions that will separate specialized law firm accounting solutions from generic bookkeeping:

Question 1: Have you worked with law firms before?

This matters more than you think.

Law firms have unique cash flow patterns, billing structures, and compliance requirements that other businesses simply don't deal with. Someone who understands cash flow from a practice area perspective will serve you more effectively than a bookkeeper who doesn't understand the different ways that law firms make money and protect profits.

Take the cash flow volatility a personal injury firm experiences, for example. That's a completely different model than what a trust and estate firm would experience. Understanding these nuances is critical for proper bookkeeping for lawyers.

Question 2: Are you familiar with trust accounting and matter-level reconciliation?

A bookkeeper must understand a few key facts when accounting for trust transactions:

Number one: The money in trust is not considered revenue until it is earned, billed, and physically transferred to the firm's bank account.

Number two: The nature of client advanced costs and how to account for them properly.

Number three: Each state has its own set of rules and requirements on how to handle trust transactions.

If they can't speak confidently about three-way reconciliations and IOLTA compliance, keep looking.

Question 3: Are you willing to access our databases to collect the information you need to perform a three-way trust reconciliation?

If a bookkeeper is relying on you to manually send them all the supporting data, they're not willing to go above and beyond to take work off your plate.

A specialized team will access your tech platforms to collect the data they need to accurately account for trust transactions. This also serves as a control between the books and your team, ensuring that both sets of data agree at all times. They can catch entry errors and give you the opportunity to work with your team before big mistakes are made.

Question 4: If you come across a trust transaction that lacks data, what are your protocols?

Here's a big one.

It's not uncommon to come across trust transactions that have no documentation or notes, meaning we have no clue which matter that transaction belongs to. The question is: what does your bookkeeper do about it?

A reactive bookkeeper will leave it on the sidelines and hope you notice. A proactive bookkeeper will have a process for getting those items out of "three-way purgatory" and attached to their matter ASAP.

It's the difference between doing the bare minimum and going above and beyond.

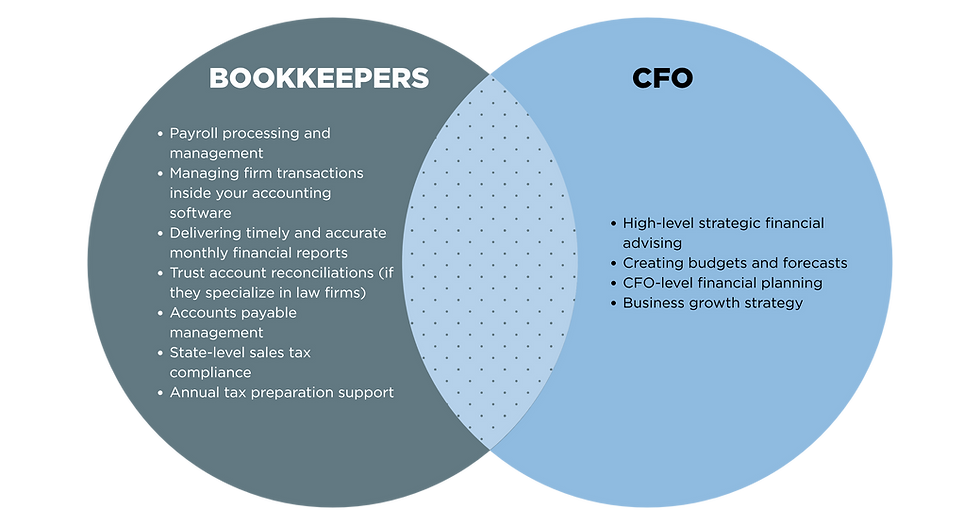

Understanding What Bookkeepers Do (And What They Don't)

Let's clear up some confusion about what you should expect from bookkeeping services for law firms.

What Bookkeepers ARE Responsible For:

Payroll processing and management

Managing firm transactions inside your accounting software

Delivering timely and accurate monthly financial reports

Trust account reconciliations (if they specialize in law firms)

Accounts payable management

State-level sales tax compliance

Annual tax preparation support

What Bookkeepers Are NOT Responsible For:

High-level strategic financial advising

Creating budgets and forecasts

CFO-level financial planning

Business growth strategy

Here's our take: if the same person does your bookkeeping AND claims to provide high-level advisory services, they're probably not great at either. Bookkeeping means keeping up with the basic requirements of financial data management and reporting.

That said, at Core Solutions Group, we offer both specialized law firm bookkeeping services AND fractional CFO services, but they're separate offerings with different team members and different focuses. This ensures you get expert-level execution on both fronts.

If you need strategic guidance alongside your bookkeeping, look for a firm that offers both services separately rather than trying to get everything from one person wearing too many hats.

Want to learn more about the difference between bookkeeping and CFO services? Check out our blog: Why You Should Not Take Business Advice from Your Tax Preparer

What You Actually Need from a Bookkeeper

Understanding your own needs is what will help you find the right fit. Here's what you might need from bookkeeping services for law firms:

☐ Catching up the books for months or years so you're current

☐ Monthly bookkeeping with consistent, reliable reporting

☐ Monthly three-way trust reconciliation on IOLTA account(s)

☐ Monthly financial reports that actually make sense

☐ Payroll processing and compliance

☐ State-level sales tax management

☐ Accounts payable management to keep vendors paid on time

Be clear about what you need before you start interviewing candidates. This clarity will help you find law firm accounting solutions that actually fit your practice.

The Team vs. Solo Bookkeeper Debate

Question to Ask: Who will be working on my account?

There are two schools of thought on this topic, and both have merit.

The Solo Bookkeeper Approach:

Some law firm owners prefer one person to have access to their financial data. We understand it's not easy to hand over all your banking information, passwords, and access to the most private matters in your business. It takes vulnerability to allow even one person behind the curtain of your law firm finances.

If you prefer the one-person approach, here's one key tool that will minimize risk: Request that your bookkeeper maintain an accounting systems manual detailing all of the tasks and frequency that go into your books.

This way, if something happens (they get sick, quit, or worse), you're not left trying to piece together their processes.

The Team Approach:

The benefits of having multiple people who are familiar with how to maintain your books far outweigh the perceived benefits of having one person. Here's why:

No single point of failure if someone gets sick or leaves

Quality control through multiple sets of eyes

Specialized expertise (one person handles payroll, another handles trust accounting)

Consistent service without interruption

At Core Solutions Group, we use a team approach because we believe your financial management is too important to depend on one person.

Protecting Your Sensitive Information

Question to Ask: What are your internal systems to protect my information?

Hiring a bookkeeper is equivalent to hiring a housekeeper. They have the keys to your financial house and access to all the rooms, valuables, and information you keep in your home.

You MUST be willing and able to trust them because the hard truth is, they could mishandle your information and your assets. Scary, right?

As with any other risk associated with being a business owner, you can minimize and manage this risk by asking the right questions.

Questions to ask about data security:

How do you protect my sensitive information?

Who has access to this information?

Do you have internal controls and security protocols?

If they can't answer all three questions with systematic, detailed answers, your data may be at risk.

The Delivery Timeline Question

Question to Ask: When will I receive monthly financials?

The age-old "I have a bookkeeper but I never see financials" problem.

You should get what you pay for, and the most valuable deliverable your bookkeeper is responsible for is your monthly financial statements. You should receive them:

Consistently, every single month

Preferably by the 15th of the following month

In a format that's easy to understand and actionable

If your provider has solid systems in place for their business, timely delivery won't be an issue.

The Top 3 Mistakes That Will Cost YOU Money

You are partnering with your bookkeeper. The quality of any partnership hinges greatly on communication.

Bookkeepers are not magical mind readers. Even if you hand them all the shoeboxes of receipts and random financial documents, they should still have questions. Your frustration often comes from a place of avoidance toward your financial data, and that's on you, business owner.

Resisting the process is costing you everything you're working toward.

Especially if you're transitioning from no books to monthly bookkeeping, recognize that building your financial foundation takes time and grace on both your part and your bookkeeper's part. On average, it takes three to six months for your accounting systems to become a well-oiled machine that produces consistent, quality results.

We have to shift the way you think about this partnership so you can avoid these detrimental mistakes:

Mistake #1: Thinking you don't need to be involved

The quality of your financial data will reflect the quality of time and involvement you give it. Period.

Mistake #2: Thinking one mistake warrants firing your bookkeeper

We call this "bookkeeper hopping." Perfection is no more attainable for your bookkeeping team than it is for you. Mistakes will happen; how they are remedied is what matters.

Mistake #3: Thinking your bookkeeper is your financial advisor

That's like asking your receptionist to litigate your trial. There, that should make sense now.

If these new schools of thought challenge you, consider this: the only way to grow and scale a profitable law firm is through delegation and management. If you're having problems here, it's almost certain you're having the same problem delegating in other areas of your business.

Where to Look for a Bookkeeper (The Rule of Three)

We encourage you to use the Rule of Three.

The Rule of Three states that you should interview at least three potential candidates because good fit matters. Understand your options and don't settle with the first one you talk to. This ensures a more informed decision-making process, helping you find the best law firm bookkeeping services tailored to meet your firm's financial needs.

Once you've compiled a list of three prospective bookkeepers, it's time to conduct interviews. We've given you all the questions to ask, so go into these meetings prepared.

Why Core Solutions Group Stands Out

Look, we're confident in what we do because we've built our entire business around serving law firms like yours.

Here's what makes us different:

We specialize exclusively in law firm accounting solutions. We're not trying to serve every type of business; we know law firms inside and out.

We understand trust accounting at a deep level. Our team performs three-way reconciliations monthly and catches compliance issues before they become violations.

We use a team approach. Your books are never dependent on one person, which means consistent service and expert oversight.

We offer both bookkeeping AND CFO services. When you're ready to level up from basic bookkeeping to strategic financial planning, we can support that growth without you having to find a new provider.

We deliver on time, every time. You'll receive your monthly financials by the 15th, consistently.

Ready to Stop Stressing About Your Books?

If you're tired of:

Wondering whether your books are actually accurate

Worrying about trust account compliance

Spending your weekends trying to figure out QuickBooks

Working with a bookkeeper who doesn't understand law firms

...it's time to make a change.

Download our free Bookkeeper Hiring Checklist to make sure you're asking all the right questions and avoiding red flags:

Or, skip the search entirely and work with a team that specializes in legal bookkeeping and law firm accounting solutions.

The Bottom Line on Finding a Law Firm Bookkeeper

Finding the right bookkeeper isn't just about finding someone who can balance your accounts. It's about finding a partner who:

Understands the unique compliance requirements of law firms

Proactively manages your trust accounting

Delivers consistent, timely financial reports

Frees you up to focus on practicing law and growing your firm

Don't settle for a generic bookkeeper who's learning law firm accounting on your dime. Your practice and your license deserve better.

Not sure if you should outsource or hire an in-house bookkeeper? We've got a blog for that:

About the Author

Chelsea Williams is the Chief Financial Architect at Core Solutions Group, where she has specialized in law firm financial management for over 8 years. She works exclusively with law firm owners to implement strategic financial systems, master trust accounting compliance, and build profitable, sustainable practices. Chelsea's expertise encompasses IOLTA reconciliation, cash flow management, and fractional CFO services tailored to the specific needs of the legal industry. Her approach combines hands-on financial operations with strategic planning to help law firm owners achieve financial freedom without sacrificing work-life balance.